In previous months, we have examined various topics such as the taxation of Social Security benefits, pre-tax vs. post-tax accounts, and the risk of sequence of returns. This month, we’ll examine inflation risk and longevity risk.

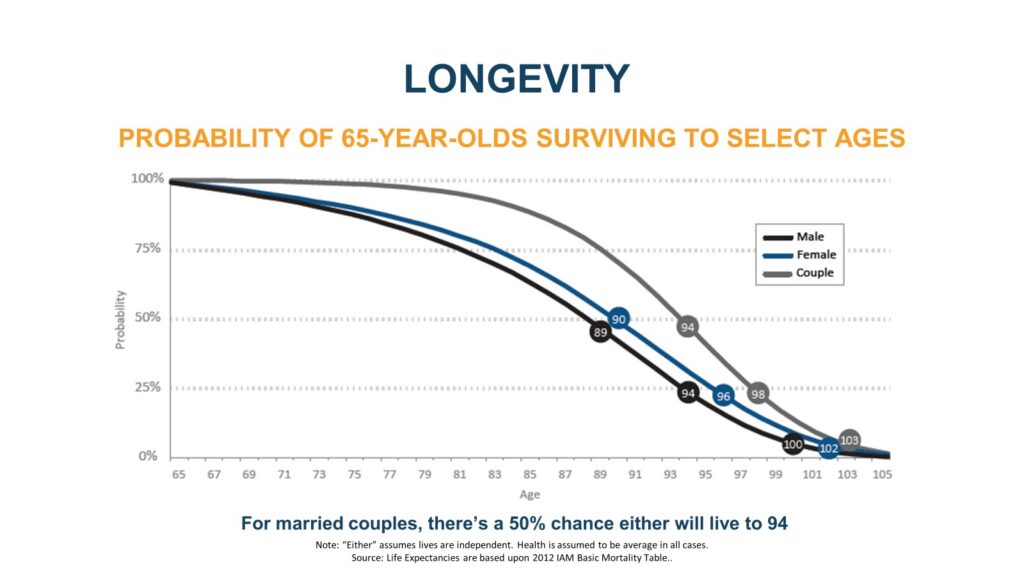

Inflation is a hot topic right now. It affects everyone (it’s been called the “universal tax”, as everyone pays for it), and can have a drastic impact on your retirement income. The average inflation rate in the U.S. over the past one hundred years is a little over 3%/year. That may not sound like a big deal, but at 3%+ annual inflation you need your income to double every twenty-two years to keep up with purchasing power of today. Depending on how old you are when you retire, you have to account for a 20-, 30-, or even 40-year retirement. Part of what we do is manage expectations, and in general, people are going to live longer than they expect. If you are married and 65 years old today, there is a 50% chance one of you will be here at age 94. Due to advances in modern medicine, lifestyle, etc., it is highly likely that age expectancy will continue to increase from here. While Social Security provides cost of living increases to help combat inflation, the majority of pensions (if you’re lucky enough to have one), are level. Therefore, it is crucial to make sure you have other sources of income that have the ability to increase (or investment accounts to pull additional income from) in order to help offset inflation.

On top of having a proper estate plan (will, power of attorney and healthcare powers), it’s very important to review beneficiary designations to assure you have both primary and contingent beneficiaries on your life insurance contracts, retirement plans (401K’s, IRA’s, 403B’s, etc.) and annuities. This is an often overlooked, but extremely impactful estate transition tool. If beneficiary designations aren’t done properly, it can create a “tax bomb” and prevent your heirs from stretching the tax obligation of an Inherited IRA over ten years and pay at the highest bracket.

Some of our clients want to maximize what goes to their beneficiaries and leave a legacy, as long as they have what they need to live comfortably. Other clients want to enjoy all their money and have the last check they write to “bounce”. Whatever your goals, we can help you achieve them with a written, cohesive, holistic strategy that encompasses estate, retirement income, money management, insurance, etc., and not just one aspect of your finances. If you have some parts taken care of already and only need help with one aspect, we are happy to help with that, as well.

Call us if you’d like to explore all your options or if you’d just like a “second set of eyes” of what you’ve put in place so far, with no obligation. The only two outcomes of getting together are a peace of mind that you’re in great shape, or we may uncover an issue that you may not be aware you had, and you can decide how or if you want to address it.

If you missed the previous month’s articles on pre-tax vs. post-tax and Sequence of returns risk and would like to receive them, please email my office manager, Jen Wukits, at jwukits@regalria.com, and we’ll be happy to email them to you.

Investment advisory services offered through Regal Investment Advisors, LLC, an SEC Registered Investment Advisor. Registration with the SEC does not imply any level of skill or training. Bailley Group Wealth Management is independent of Regal Investment Advisors.