How Do Taxes Affect Investment Portfolios?

A variety of taxes can affect net investment results. Securities sold at a gain are subject to capital gains taxes at ordinary income tax rates if held for longer than a year, or at lower long-term rates if held longer than a year. Dividends are subject to tax, either at the dividend tax rate if they are qualified, or at the ordinary income tax rate. Interest payments are also taxed as ordinary income, although municipal bond interest payments may be exempt from certain taxes. State taxes, if applicable, can also come into play.

How can investors reduce taxes on their investments?

One of the most effective techniques is tax-loss harvesting. Typically, a financial advisor assesses a client’s realized gains toward the end of the year and then looks for portfolio positions with unrealized losses. These can be sold to realize the losses, which can be used to offset realized gains and a small amount of ordinary income. While this is helpful, waiting until year-end has significant shortcomings. For example, if the market dips early in the year but rebounds strongly by November or December, there may be few losses to harvest.

Another disadvantage is that annual loss harvesting may require selling off large portions of assets to offset realized gains, which can cause the portfolio to perform differently than intended. The better approach to loss harvesting is to do it throughout the year and in a risk managed way. Quantitative tools can be used to evaluate potential differences in portfolio returns incurred by selling positions and weigh them against the tax benefit of harvesting those positions.

What other techniques can help reduce tax liability?

Key techniques include:

- Deferring sales on securities with short-term gains until they qualify for the lower long term capital gains rate

- Choosing the optimal tax lot when selling a security to reduce tax liability

- Avoiding violations of the IRS wash sale rule, when appropriate, which disallows the use of a realized loss if the same or a substantially similar security is purchased within 30 days

- Using additional contributions rather than selling securities (which can generate taxable gains) to rebalance portfolios

Research has shown that taxes can cost investors as much as 2% or more in return on an annualized basis.1, 2, 3 Lipper Analytics has observed that taxes are at least as important as fees in terms of their impact on investor returns.4 Surprisingly, however, many investors and their financial advisors pay little attention to taxes when making investment decisions.

How much benefit can be generated using these techniques?

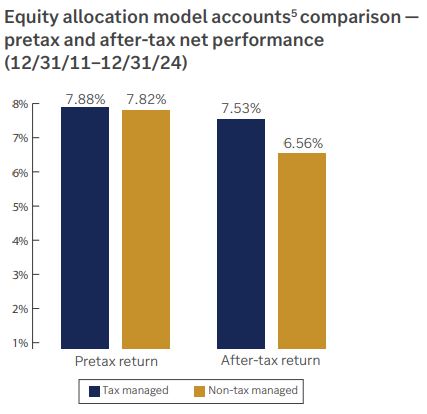

The following chart shows the results for a pair of portfolios managed for 13 years by Edward Jones’ overlay management team. Both used the same investment strategies and vehicles, target allocations and rebalancing, but one also employed tax management techniques. Pretax, there is very little difference in the portfolio returns — just 0.06% on an annualized basis. But the difference in after-tax returns is substantial, at 0.97% annually.

These results assume no final liquidation of the portfolios at the end of the period, which would reduce the difference. The magnitude of this benefit also depends on other factors, including:

- The market environment, as more volatile markets create more opportunities to tax-loss harvest.

- The overall allocation to equities, which offer more tax management potential than other assets.

- The use of separately managed accounts (SMAs), which provide more flexibility for customization, including tax management.

How common is tax management?

Unified managed accounts (UMAs) that combine SMAs, mutual funds and exchange-traded funds (ETFs) have greatly increased the prevalence of tax management for several reasons:

- In SMAs, UMA investors establish their own cost basis, or original asset value, in the securities they buy, avoiding the embedded capital gains associated with funds. Owning individual stocks also presents more opportunities for tax-loss harvesting.

- Overlay managers (specialists in implementing multi- strategy UMAs) are well-positioned to execute tax management techniques because they coordinate activity across the entire portfolio. This makes it easier to ensure wash sales don’t interfere with loss harvesting and that optimal tax lots are selected when selling positions.

- Sophisticated overlay managers may also have the tools and experience to capitalize on opportunities for reducing tax liability without significantly affecting the pretax performance of the portfolio.

Clients should always consult with their tax advisor to discuss their personal situation. The information provided here is for informational purposes only and should not be considered a recommendation for investment action.

To learn more about how we can implement tax efficient strategies in your portfolio, contact me today.

7708 N Grand Prairie Drive

Peoria, IL 61615

309-691-3238

1 J.D. Peterson, P.A. Pietranico, M.W. Reipe, and F. Xu, “Explaining After-Tax Mutual Fund Performance.” Financial Analysts Journal, Vol. 58, No. 1 (January/February 2002).

2 Longmeier, G. and G. Wotherspoon, “The Value of Tax Efficient Investments: An Analysis of After-Tax Mutual Fund and Index Returns.” The Journal of Wealth Management, Fall 2006.

3 Peterson, J.D. and R. Spiegelman, “The After-Tax Performance of Mutual Funds: Why It’s Important.” Schwab Center for Financial Research, September 2, 2003.

4 Lipper Analytics 2010 Tax Study, Tom Roseen, Lipper, a Thomson Reuters Company.

5 The two tracking accounts examined in this case study were both invested in portfolios composed of identical asset allocations and the same combination of SMAs, mutual funds and ETFs. The pair began with identical portfolios and the same cost basis and purchase date for the underlying securities. The tracking accounts were all invested in accordance with asset allocation models used for actual client accounts. Changes to asset allocations, manager changes and trades in the underlying separate account strategies were all implemented consistently with the manner and timing that they were implemented in actual client accounts. Asset class drift monitoring and rebalancing as well as loss harvesting for the tax-managed tracking accounts were also conducted in the same manner that they were for actual client accounts. Since the tracking accounts were paper portfolios and did not represent actual assets, the trade execution was simulated. Trades for the tracking accounts were generated at the same time these trades were generated for actual client accounts. Instead of these trades being actually executed as they were for actual client and seed accounts, however, these trades were assumed to be executed at the current market price of the security being traded. Returns are net of a maximum fee rate of 1.89%. The projections and illustrations shown are hypothetical in nature, do not reflect actual investment results and are provided for informational purposes only. They should not be used or relied upon to make decisions. The performance of these hypothetical illustrations might have been worse if these factors had been considered. Nothing herein is intended as specific investment advice, and no person should make any investment decision based solely on the information contained in this communication. Clients should always consult with their tax advisor to discuss their personal situation. Edward Jones, its employees and financial advisors cannot provide tax or legal advice. The investment strategies mentioned may not be suitable for everyone. Results may vary. Tax alpha is the incremental benefit associated solely with active tax management. Edward Jones is a dually registered broker-dealer and investment adviser. Edward Jones offers the Overlay Management Services exclusively to clients of the Edward Jones Advisory Solutions® Unified Managed Account advisory program and Investment Advisory Program. More information on these advisory programs and overlay management services is available at edward- jones.com/advisorybrochures.