How to Manage Your Sequence of Returns Risk

In my last article, we looked at the difference between pre-tax and post-tax accounts during the savings years. This month, we’re going to start exploring risks that are present during the income years, that aren’t there during the savings years, that you may not be aware of. We like to compare the savings years to playing checkers, a relatively simple board game that families can play together. But the day you retire and have to start spending out of a portfolio, you graduate from playing checkers to chess. The board may look the same (the market), but many risks come into play that weren’t there during the savings years, such as sequence of returns risk, withdrawal rate risk, longevity risk, etc. We’re going to be exploring those over the next few months.

Sequence-of-Returns Risk

If you took $100,000 and put it in the market and had a specified period of time (let’s say 10 years), and averaged 7%/year, it wouldn’t matter what the sequence was (year-by-year returns, as long as they both average the same annual rate). You’d end up with almost $200,000 after 10 years, regardless of the sequence. But what if you start taking withdrawals from that portfolio because you’ve now retired and need income from it? In my opinion, money should be managed differently for growth than for income.

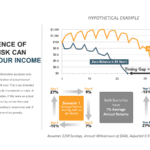

Take a look at the example below. In scenario one (where you had positive returns in the first few years of withdrawals), your money lasts for 37 years, which is fantastic! But look at scenario 2 (you experience down markets in the early years of withdrawal). You run out of money 13 years sooner. Remember, both portfolios averaged 7%. But once you start spending out of a portfolio, the average rate of return becomes meaningless because of sequence-of-returns risk.

Part of the problem that contributes to sequence-of-returns risk is when you are using your whole portfolio to generate your income. In my experience, it’s the most common way that retirees (and their advisors) structure their retirement income plan. When you use your whole portfolio and apply a withdrawal rate for income (4%, for example), you are relying on positive market returns (and hope) to make your money last. Another issue with that approach is that you need your whole portfolio to generate your income, so it truly isn’t “liquid” (meaning if you needed a lump sum withdrawal for something, you now have less in your portfolio to generate your needed income stream). There are other (and better, in my opinion) overall retirement and income strategies that we utilize to be as efficient as possible. As I’ve mentioned in previous articles, every situation is different and there is no “magic bullet” that works for everyone. All of our strategies are tailor-made to you and your situation. Give us a call and we’d be happy to discuss how we can help.

Investment advisory services offered through Regal Investment Advisors, LLC, an SEC Registered Investment Advisor. Registration with the SEC does not imply any level of skill or training. Bailley Group Wealth Management is independent of Regal Investment Advisors.

Any content, resident submissions, guest columns, advertisements, and advertorials are not necessarily endorsed by or represent the views of Best Version Media LLC (BVM) or any municipality, homeowners associations, businesses, or organizations that this publication serves. BVM is not responsible for the reliability, suitability, or timeliness of any content submitted, inclusive of materials generated or composed through artificial intelligence (AI). All content submitted is done so at the sole discretion of the submitting party.