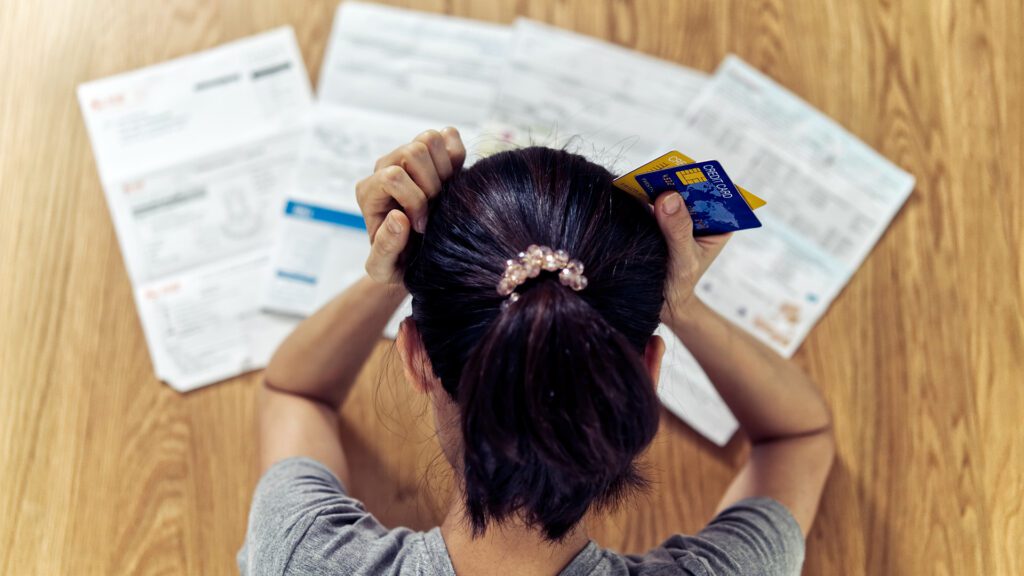

Every Mar. or Apr., I inevitably overhear a conversation while standing in line somewhere: “Well…I guess we’ll see what we owe.” That’s the narrative that many Americans take, when it comes to their taxes. It’s that sinking feeling of opening your mailbox and hoping not to see a letter from your accountant saying that you owe much more than you were anticipating. No one likes that feeling. It feels like a pop quiz you didn’t study for, except this one can cost five or six figures. By the time you know the number, it’s too late to change it. The income is earned. The calendar is closed. You’re not planning anymore; you’re just reacting.

Tax season doesn’t have to feel that way.

The feeling of relief happens when you look at them before Dec. 31. Instead of guessing, you model it out. What does this year look like, if you do nothing? What happens if you convert a portion to Roth? Should you harvest losses? Realize gains? Accelerate income? How close are you to the next marginal tax bracket? What about Medicare income-related monthly adjustment amount (IRMAA) surcharges two years from now? When you see the impact in advance, you move from anxiety to clarity.

This is something that we regularly help clients navigate—not in Apr., but in the fall. When you can see the numbers ahead of time, you regain control and can choose to act.

I also encourage people to zoom out beyond just this year. Sometimes paying more taxes now is actually the smarter move. If you’re in a relatively low bracket today, but sitting on large pre-tax retirement accounts, future required minimum distributions (RMDs) can create a much bigger tax problem later (not to mention potentially creating higher Medicare premiums). Intentionally paying tax at 22% today may be far better than being forced to pay 32% in retirement. That’s the difference between short-term thinking and having a lifetime strategy.

And then there are investments! Two investors can earn the same return; but one loses more to tax drag, simply because no one reviewed the tax efficiency of their holdings. Asset location, turnover, capital gain distributions—they matter more than people realize. In the industry we call this planning for tax alpha, because it isn’t just about what your investments make, but also about what you get to keep.

Apr. is for filing. Dec. is for deciding. And the difference between those two mindsets compounds over time.

Let Anderson Financial Strategies be your tax knowledge tutor. Contact us at andersonfinancialstrategies.com or 937-610-9388.

Any content, resident submissions, guest columns, advertisements, and advertorials are not necessarily endorsed by or represent the views of Best Version Media LLC (BVM) or any municipality, homeowners associations, businesses, or organizations that this publication serves. BVM is not responsible for the reliability, suitability, or timeliness of any content submitted, inclusive of materials generated or composed through artificial intelligence (AI). All content submitted is done so at the sole discretion of the submitting party.