Any seasoned investor will tell you that trying to time the market is a fool’s errand. Many have tried and failed to select the perfect time to buy and sell a stock. With this fact in mind, dollar-cost averaging is an investment strategy that all investors, especially risk-adverse ones, should strongly consider. Dollar-cost averaging is the practice of investing equal or fixed amounts of money at regularly scheduled intervals instead of a lump sum.

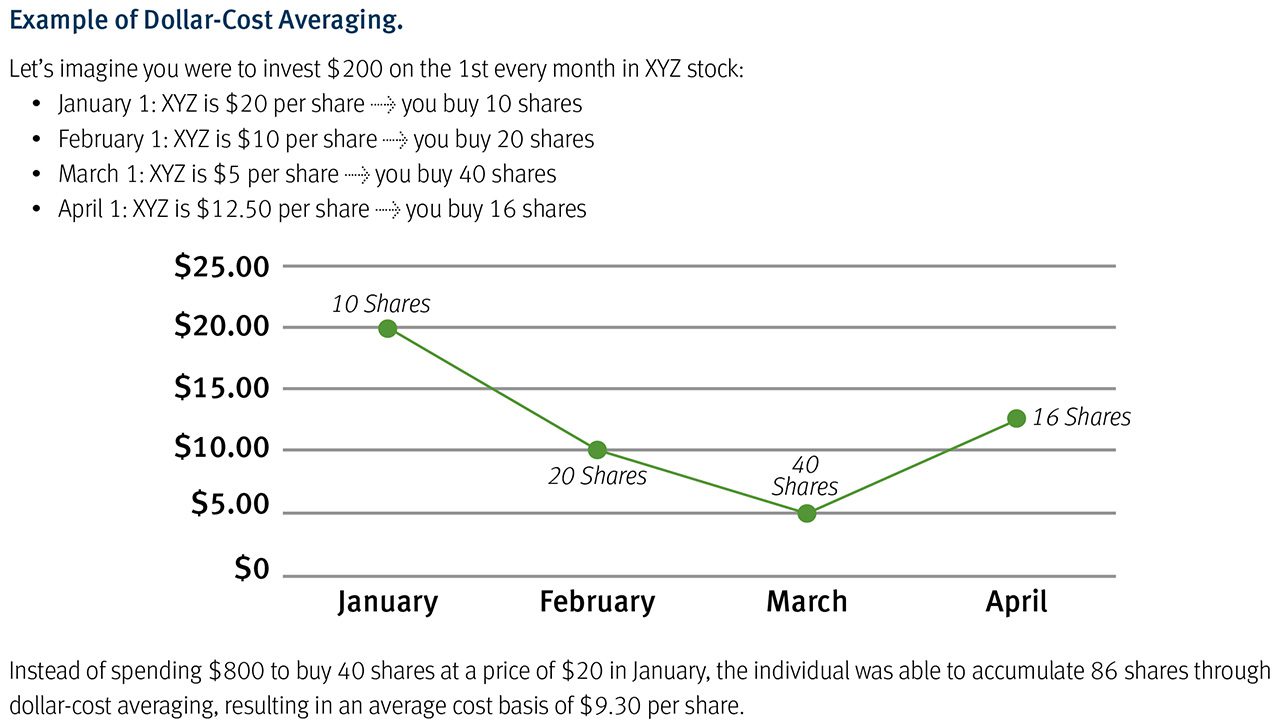

For example, if you have $5,000 to invest, instead of using it to buy a bunch of shares of a stock in one fell swoop, you can instead utilize dollar-cost averaging and invest $1,000 a month for five months or $500 a month for 10 months. By employing this strategy, your money will buy more shares when the market value of your investment is low and fewer shares when the value is high. This may help you mitigate risk since you won’t risk investing a large sum of money at the wrong time. In addition, dollar-cost averaging forces you to invest on an ongoing basis, so you aren’t compelled to sell when the market is low or buy when it goes up. The fact that you invest continuously also makes dollar-cost averaging a suitable strategy for long-term goals such as retirement.

If you have a workplace 401(k) plan, you are already taking part in dollar-cost averaging because your contributions are allocated to specific investment options through automatic payroll deductions that occur on a regular, fixed schedule.

No single investment strategy is a golden ticket. They all have their benefits along with potential downsides, and dollar-cost averaging is no different. This strategy forces you to hold on to your investable sum of cash to invest in increments instead of all at once which, despite the many benefits we outlined above, can prevent it from growing as much as possible. You may also have additional brokerage fees to contend with since dollar-cost averaging requires a series of ongoing transactions. These fees, if applicable, will reduce your earnings. In short, dollar-cost averaging does not assure a profit or protect against a loss.

As with any investment plan, dollar-cost averaging isn’t for everybody. To determine if it’s for you, ask yourself the following questions:

- What is my tolerance for risk?

- Am I comfortable investing during periods of stock market turbulence?

- Am I willing to sacrifice higher potential returns for a steady, lower-risk approach?

Anytime you’re considering implementing an investment strategy, it’s always wise to consult with your financial advisor. Before moving forward, set up a time to talk with your financial professional to determine if dollar-cost averaging makes sense for your financial profile, desired goals, and time horizon.

Article provided by Robert Cleary, Senior Vice President/Investments, with Stifel, Nicolaus & Company, Incorporated, member SIPC and New York Stock Exchange, who can be contacted at Stifel’s 3 Bryant Park office at (212) 847-6517.

Dollar-cost averaging does not assure a profit or protect against a loss. Investors should consider their ability to continue investing during periods of falling prices.

Rebalancing may have tax consequences, which you should discuss with your tax advisor.

Sources:

“The Pros and Cons of Dollar-Cost Averaging,” FINRA, March 24, 2022, https://www.finra.org/investors/insights/dollar-cost-averaging

Hayes, Adam, “Dollar-Cost Averaging (DCA) Explained With Examples and Considerations,” Investopedia, May 23, 2024, https://www.investopedia.com/terms/d/dollarcostaveraging.asp

Any content, resident submissions, guest columns, advertisements, and advertorials are not necessarily endorsed by or represent the views of Best Version Media LLC (BVM) or any municipality, homeowners associations, businesses, or organizations that this publication serves. BVM is not responsible for the reliability, suitability, or timeliness of any content submitted, inclusive of materials generated or composed through artificial intelligence (AI). All content submitted is done so at the sole discretion of the submitting party.