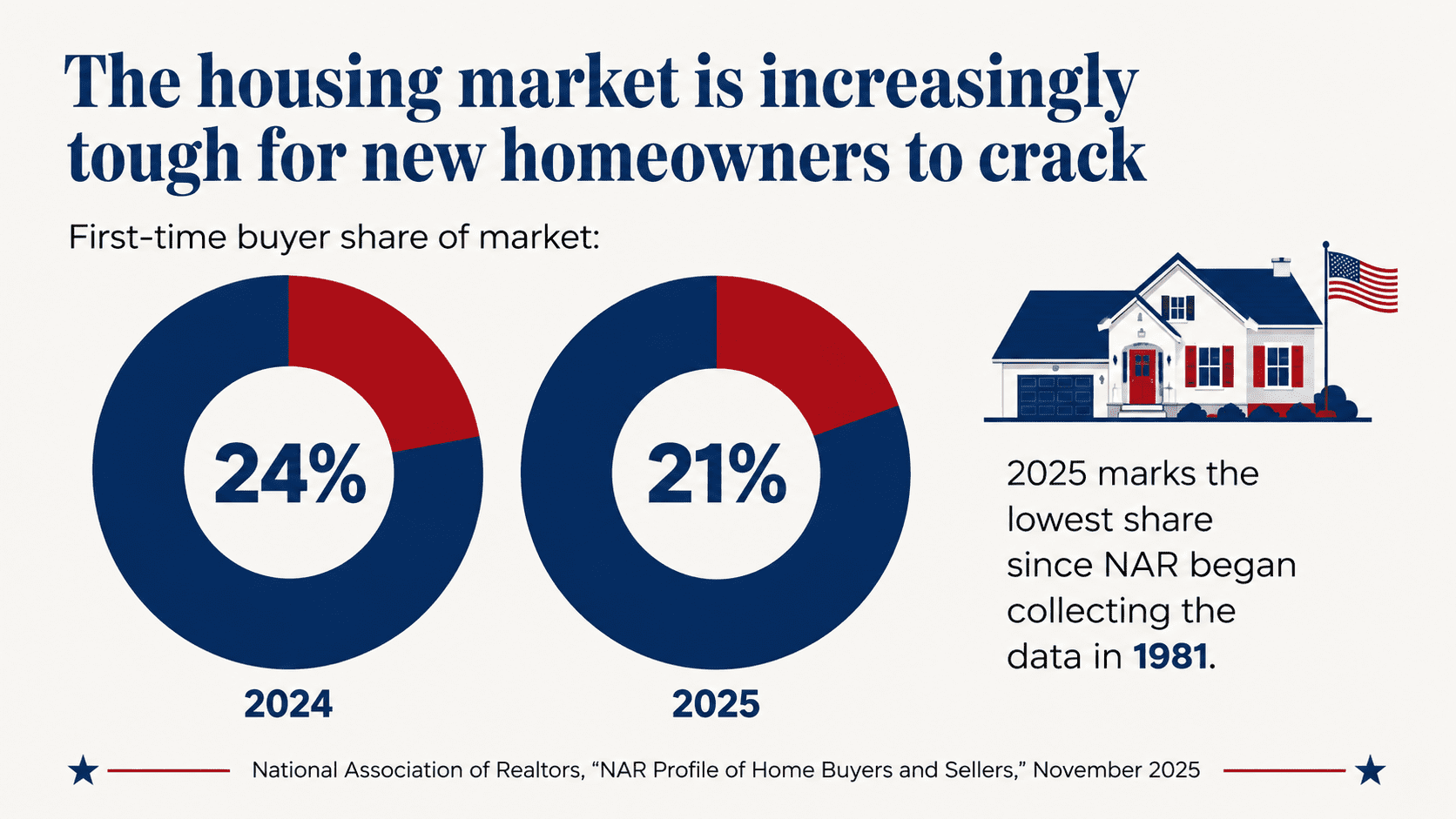

According to the National Association of Realtors, the typical first-time buyer is now 40 years old, and first-time buyers account for just 21% of home purchases — the lowest level on record.

Supporting Homeownership With a Thoughtful Plan

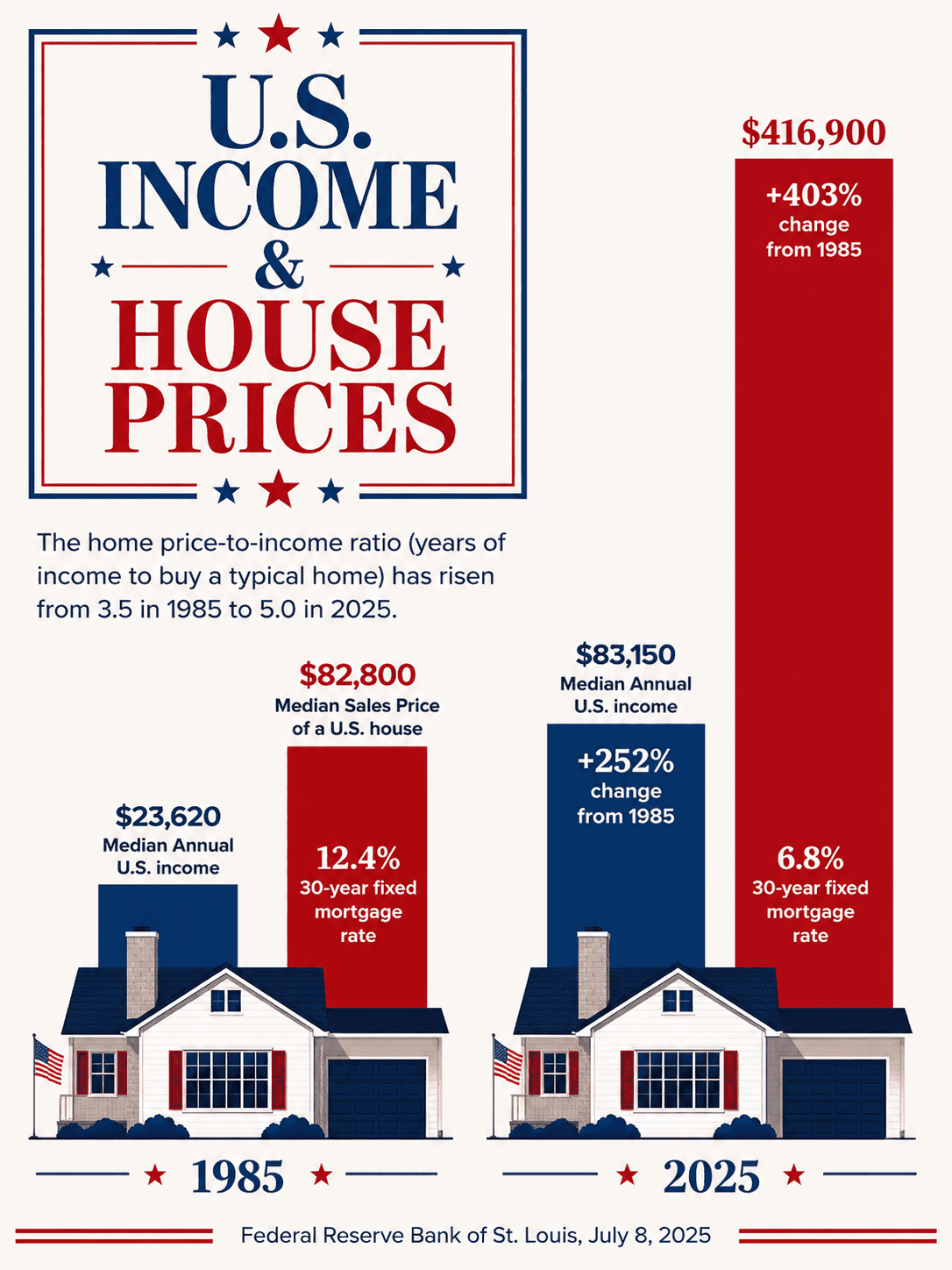

For many parents and grandparents, seeing their children and grandchildren struggle to buy a home can feel frustrating. Despite working hard and earning solid incomes, many first-time buyers are delaying homeownership because of rising prices, higher mortgage rates, student loans, and the growing cost of everyday life.

As affordability challenges grow, more families are stepping in to help. Nearly a quarter of first-time buyers now rely on financial support from family members for down payments.

If you are considering helping a child or grandchild buy a home, there are several approaches worth evaluating. Some families choose a straightforward cash gift, while others prefer structuring support as an intra-family loan with clear repayment terms.

Other options may include co-owning the property, using a trust or LLC to hold ownership, or gifting an existing property. Each option comes with its own financial, legal, tax, and estate-planning considerations.

Questions to Consider Before Offering Financial Help

- Can you comfortably afford the support (without impacting your own long-term goals)?

- Should the assistance be considered a gift, a loan, or an investment?

- How should the arrangement be documented?

- Are there ways to help protect the asset in the event of divorce or future disputes?

- How does the decision fit into your broader estate strategy and fairness among children or grandchildren?

Helping with a down payment can be about far more than simply writing a check. It can become part of a thoughtful multi-generational wealth strategy designed to create opportunity, stability, and long-term financial confidence for future generations.

To discuss ways to help children or grandchildren purchase a home while maintaining a smart long-term financial strategy, connect with the Yardley Wealth Management team.

You can also read the full article and detailed strategies at bit.ly/YWM-down-payment.

Any content, resident submissions, guest columns, advertisements, and advertorials are not necessarily endorsed by or represent the views of Best Version Media LLC (BVM) or any municipality, homeowners associations, businesses, or organizations that this publication serves. BVM is not responsible for the reliability, suitability, or timeliness of any content submitted, inclusive of materials generated or composed through artificial intelligence (AI). All content submitted is done so at the sole discretion of the submitting party.