There is no greater need for elder planning than when a family business is involved. An entrepreneur whom we will call Pops was married to Mom, and together they opened a family restaurant that became wildly successful. The restaurant served customers within a 100-mile radius and was often mentioned in magazines and newspaper reports, and in later years on the internet, as a place to see and be seen.

Pops wanted the business to continue as a family operation after his death. By reputation, he ruled the business with a firm hand. He had a strong personality and a strong mind for the restaurant business, but far less interest in estate planning. After Pops’ death, Mom and the three children endeavored to carry on the thriving family business, which was organized as a family-owned corporation.

Over time, Mom withdrew from the business, and the children assumed full control of operations. By then, the company had expanded beyond dine-in service to include merchandise sales and off-premises food sales. The children entered into a shareholders’ agreement that provided each child with a substantial annual distribution intended to serve as executive compensation. Approximately ten years later, two of the children decided the friction associated with the third child’s involvement could no longer be endured. They voted to suspend that child from daily operations. Within a year, the corporation stopped paying the annual distribution to the suspended child. Two years after the suspension, the ousted child developed cancer and died. What role did unresolved family conflict play in those business decisions? Did business pressures strain family relationships? These questions linger long after the decisions were made.

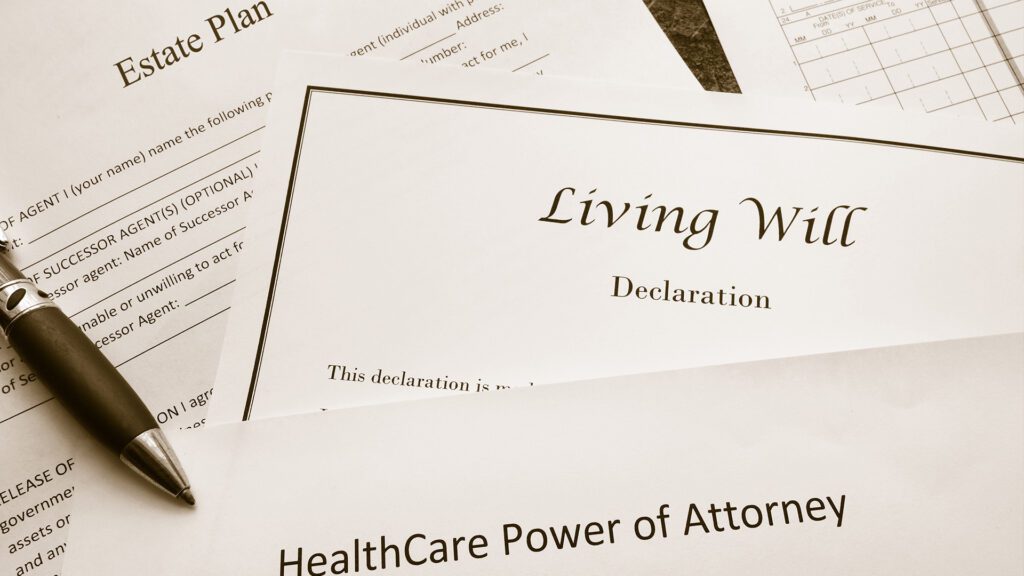

It has now been ten years since the ouster. Two lawsuits have been filed involving the children and the corporation, and a probate action has been opened to administer the estate of the deceased child. Litigation has flourished almost as rapidly as the business itself has grown. The appellate court has already reviewed one case, and further litigation is inevitable, as many issues remain unresolved. Management of the business is captive to this controversy, and legal fees continue to mount. Could this conflict have been largely, if not completely, avoided? Certainly, Pops did not engage in elder planning with the continuation of the family business or the resolution of family conflict in mind. He passed assets down to his family but put no mechanism in place to manage disputes or transitions.

Pops could have created a family trust that owned the business or held a controlling interest in it. He could have appointed someone outside the family as a trustee or tie-breaking authority when disagreements arose about who should remain involved in operations or how a family member’s interest should be liquidated in the event of death, disability, or withdrawal from the business. Corporate disputes can be bitter and long-lasting, and severing an ownership interest is often complex. Requiring family members to make corporate decisions that affect one another’s lives and incomes only compounds the difficulty. Had Pops planned his estate with the guidance of an elder law attorney, management of the business could have continued with less conflict, and the withdrawal of a family member could have been handled without the lasting burden of sibling rivalry.