When you support a cause you care about, the rewards extend far beyond the satisfaction of making a difference. The Canadian government actively encourages charitable giving through generous tax incentives that can significantly reduce your tax burden while amplifying your impact. Whether you’re gifting cash, property or securities, understanding these benefits can help you plan accordingly and give more effectively.

Gifting Guidelines

Making a personal donation to a registered charity entitles you to a valuable tax credit that reduces the amount of tax you owe. This tax credit varies and is based on your taxable income and donation amount, as well as the province or territory with which you live. The recipient(s) of this donation must also be recognized as a “qualified donee” and authorized to issue official donation receipts. Most established organizations, such as registered charities and public and private foundations, qualify. If you’re making substantial donations, be mindful of Alternative Minimum Tax (AMT), which ensures all Canadians pay minimum tax amounts. AMT calculations may reduce some advantages of donation tax credits and capital gains elimination. While there’s no limit to how much you can donate, you can generally claim donations up to 75% of your net income in a given year. Quebec residents enjoy a 100% limit, as do all Canadians in their year of death and the preceding year.

The Securities Advantage

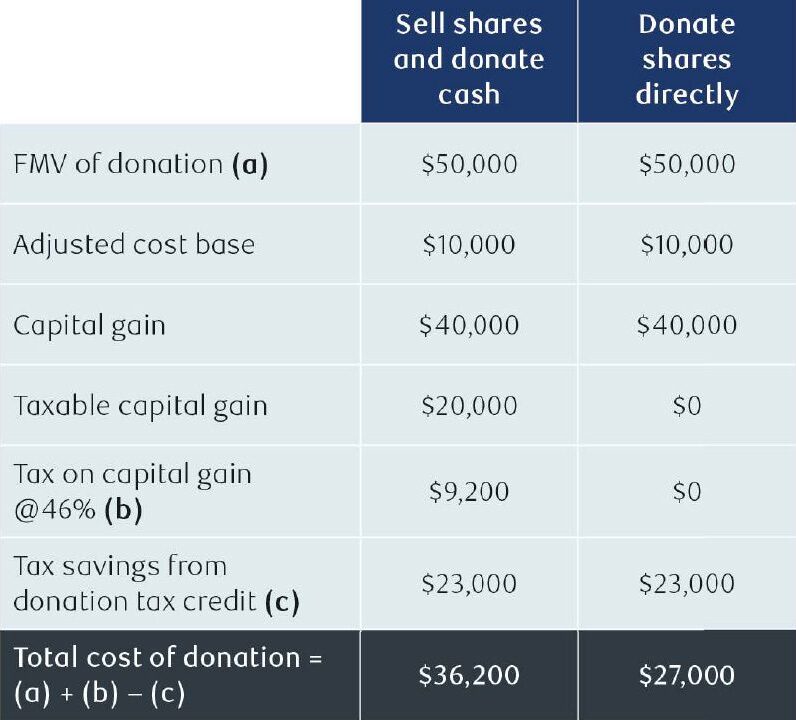

Here’s where strategic giving gets interesting. When you donate certain securities in-kind – rather than selling them first – you could eliminate capital gains tax entirely. This benefit applies to shares, debt obligations or rights listed on designated stock exchanges, mutual funds, segregated fund trust interests and government bonds. This also includes gifting appreciated property. If the property has been donated directly to a registered charity, the capital gains could be eliminated, maximizing both your donation value and your tax savings.

Donating depreciated securities in-kind is another option. This generates both a capital loss and a donation tax credit based on the current market value, which could be mutually beneficial to your tax planning initiatives as well as the receiving organization’s interests.

1. The lowest federal personal marginal tax rate is 14% beginning 2026.

2. In this example, it’s assumed that taxable income above $253,414 is subject to the top federal income tax rate of 33%; the actual amount is indexed annually.

In this example, the donor realizes savings of $9,200 ($36,200 – $27,000) by donating appreciated property instead of selling it and donating the proceeds. The difference is a result of the eliminated capital gains tax on the donated securities.

Planning Ahead

You don’t need to claim your donation tax credit immediately. In fact, you can carry it forward for up to five years, which allows you to optimize your tax strategy by claiming the credit when it provides maximum benefit.

Estate planning offers additional opportunities. When securities are donated in-kind by your estate, capital gains accrued before death may be eliminated. However, assets from registered accounts like RRSPs or RRIFs don’t receive the same capital gains treatment, as their value is taxed as income.

A Smarter Strategy

Charitable giving represents more than generosity – it’s smart financial planning. By understanding these tax advantages, particularly the benefits of donating securities in-kind, you can make your charitable dollars work harder while supporting the causes that matter most to you.

Reach out to our team today to explore how these charitable giving strategies can work for your financial plan.

Any content, resident submissions, guest columns, advertisements, and advertorials are not necessarily endorsed by or represent the views of Best Version Media LLC (BVM) or any municipality, homeowners associations, businesses, or organizations that this publication serves. BVM is not responsible for the reliability, suitability, or timeliness of any content submitted, inclusive of materials generated or composed through artificial intelligence (AI). All content submitted is done so at the sole discretion of the submitting party.