Taxes can be a significant annual expense, especially during your working years. Income smoothing is the concept of spreading taxable income across a number of years in an effort to reduce your overall taxation. The information below walks through one couple’s opportunities for reducing their total tax bill using income smoothing strategies.

Brandon and Joy retired two years ago, each at the age of 65. Prior to their retirement, their combined annual salaries totaled more than $500,000. Last year, in their first year of retirement, Brandon and Joy’s income was less than $100,000, all of which was generated by their investment portfolio. They anticipate their income will be consistent at this level until they begin receiving Social Security benefits at age 70 and start taking required minimum distributions (RMDs) from IRAs. By then, they believe their income will return to more than $500,000.

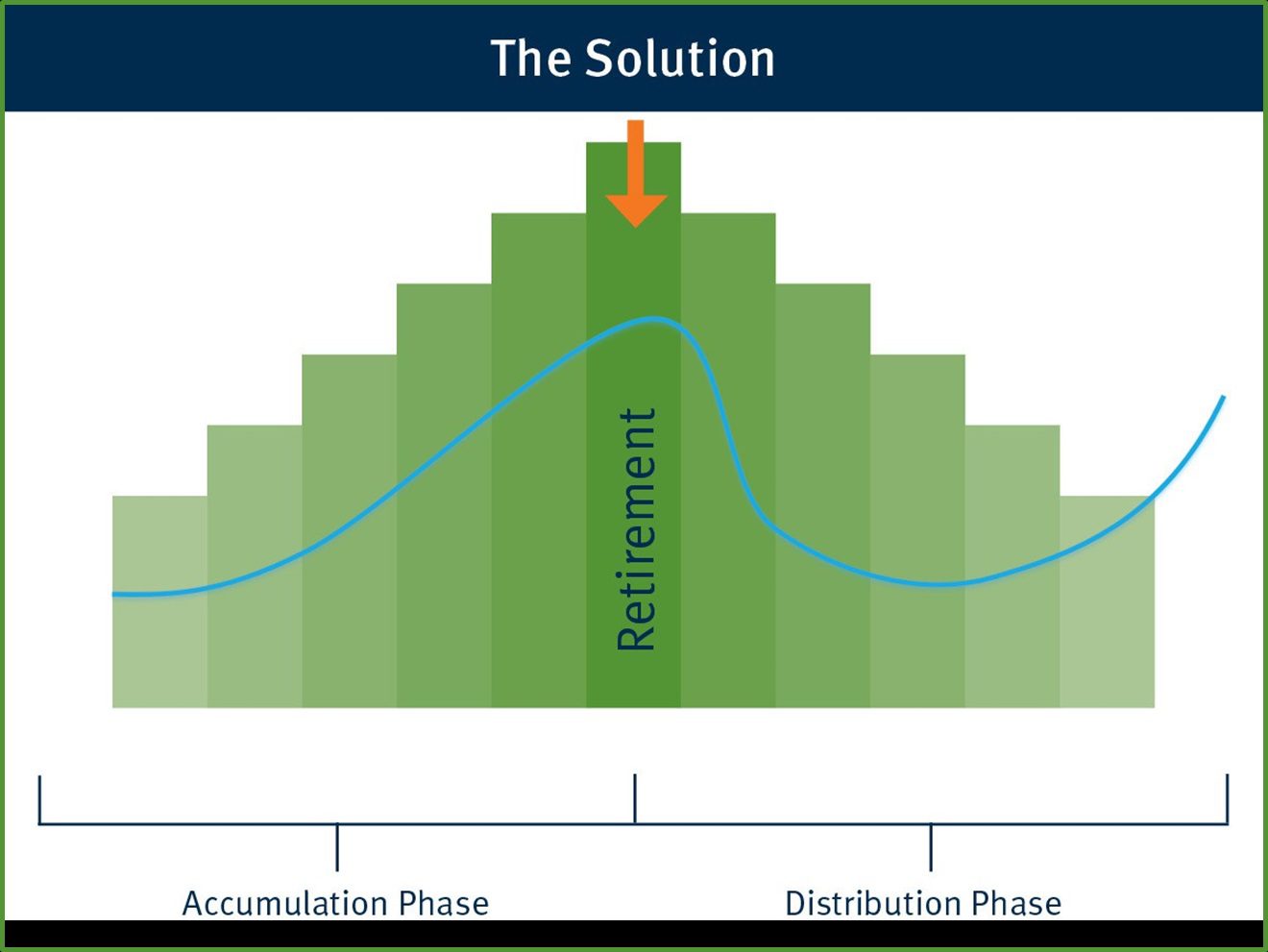

Consider the graph below. Brandon and Joy’s income – represented by the blue line – increases until they retire, drops significantly in the early years of retirement, and then climbs again once Social Security benefits and RMDs begin.

The Accumulation Phase

The accumulation phase covers the years Brandon and Joy have saved for retirement. The following strategies may have helped them reduce their taxable income during this time:

Brandon and Joy could have deferred taxation of a portion of their earned income by contributing to their pre-tax (or “traditional”) retirement plans during the final years of their careers. This would have reduced the amount of taxable income subject to the high tax rate that applied at that time.

Toward the end of this phase, it may have been beneficial to pre-fund charitable goals by utilizing a charitable trust, donor-advised fund (DAF), or other charitable giving instrument. Doing so would have allowed Brandon and Joy to take a bigger deduction during a year in which a higher tax rate applied.

The Distribution Phase

Upon retirement, Brandon and Joy entered the distribution phase, when accumulated assets are used to fund retirement. Taxpayers have some additional opportunities during the distribution phase, especially taxpayers like Brandon and Joy who see a significant drop in taxable income during their initial retirement years.

Taxpayers who have access to the 0% long‑term capital gains bracket may benefit from strategically realizing capital gains (state taxes may still apply). Even if an investor plans to hold an appreciated investment long term, realizing gains during such a year and repurchasing the investment can increase cost basis and help reduce future taxable gains. A Roth conversion is another way to fill tax brackets during a relatively low-income tax year. A Roth conversion can help level out income over time by accelerating taxation of pre-tax retirement dollars into a year when the taxpayer’s tax rate is lower than the taxpayer’s anticipated future tax rate.

Every situation is unique, and the right strategy depends on your income, assets, and long-term goals.

Article provided by Robert Cleary, Senior Vice President/Investments, with Stifel, Nicolaus & Company, Incorporated, member SIPC and New York Stock Exchange, who can be contacted at Stifel’s 3 Bryant Park office at (212) 847-6517.

This information is for educational and illustrative purposes only, is not a recommendation or investment advice, and is not indicative of future results. Individual results and circumstances will vary. Stifel does not provide legal or tax advice. You should consult with your legal and tax advisors regarding your particular situation.

Decisions to roll over or transfer retirement plan or IRA assets should be made with careful consideration of the advantages and disadvantages, including investment options and services, fees and expenses, withdrawal options, required minimum distributions, tax treatment, and your unique financial needs and retirement planning. Neither Stifel nor Stifel Financial Advisors provide recommendations with respect to your decision to move assets out of an employer-sponsored retirement plan. Once you inform your Stifel Financial Advisor that you have chosen to roll your retirement assets to an IRA with Stifel, your individual investment needs can be addressed. You should consult with your tax advisor regarding your particular situation as it pertains to tax matters.