Consider Tax Efficiency as Part of Long‑Term Financial Planning

It’s that time of year again, one that many dread. Yes, I am referring to personal income tax filing season! By the time you read this article, hopefully you’ve completed your filing or are well on your way to doing so. As a local Financial Advisor for the past 23 years, I have helped many hundreds of clients (individuals, couples, families, small business owners, professionals, executives, retirees) diligently mitigate their annual income tax burden and make income tax season a bit less painful, by pursuing consistent tax-efficient personal finance & investing strategies. I call this strategy the Tax-Efficiency mindset, because I believe when it comes to growing wealth, it’s not just about strong investment rates of return, it’s also about how much an investor keeps once taxes (both income & capital gains) are considered. If appropriate, evaluate the options below for your personal financial goals.

While one is employed, it’s important to save for the future and take advantage of tax-advantaged investing strategies. One of the most significant strategies is contributing to tax-deductible, tax-deferred retirement accounts (e.g. IRA, 401K, 403b, etc.). Health Savings Accounts are particularly attractive too, as they are both tax-deductible and tax-free for qualifying distributions. (This is why I highly recommend HSA’s if they are available through your employer.) And the tax-free Roth IRA has longer term benefits to your income tax efficiency strategies too. While Roth contributions are not deductible, they offer great tax-free growth opportunity and tax-free income with future withdrawals. There are also tax-efficient strategies which permanent Life Insurance policies can offer too.

Small business owners utilize tax-advantaged strategies not only to save for their future, but to attract & retain employees too. They do this by utilizing properly-designed retirement plans which meet their unique business & personal needs. Tax-efficient investment plan strategies apply to all types of business structures, including: sole proprietorships, partnerships and multi-employee firms. Depending upon other factors as well, small business owners and their employees may take advantage of various tax-deductible retirement plan types, including: Solo 401K, 401K, SEP IRA, SIMPLE IRA and Profit-Sharing plans. Similarly, Not-for-profit firm operators and their employees may utilize tax-deductible retirement plans too. And effective this year – given the requirements under the Secure Act 2.0 – many employers will be required to initiate retirement plans for their employees, while there are government-sponsored tax-offsets for business owners to cover some of their costs to do so.

This tax-efficiency mindset should persist even when one retires, although some of the strategies to employ may be different. In fact, many retirees are surprised to find that taxes can be the most expensive cost in retirement! By example, many retirees are surprised to discover that their Social Security income may be taxable. Thus, the focus on tax efficiency is even more imperative, when planning for retirement and once taking retirement income.

While you would always want to consult with your tax professional**, below are some strategies for retirees to consider, to maintain a tax efficiency mindset:

1. When to Take Social Security income:

- The earliest age anyone who is eligible for Social Security income is at 62 years. By delaying to a later age, this will not only increase one’s Social Security annual income benefit, it delays the tax impact of any required Social Security income tax during the period of delay.

- At least 15% of Social Security benefits are always tax-free.

- Federal taxes can be applied to up to 85% of Social Security benefits, depending on Provisional Income and filing status**.

2. Provisional Income and Taxation**:

- Provisional income determines the percentage of Social Security benefits subject to federal income tax.

- Provisional income is calculated as:

- 50% of Social Security benefits

- Plus tax-exempt (investment) interest

- Plus adjusted gross income (AGI)

- Taxation thresholds vary by filing status:

- Single filers: Up to $25,000 = 0% taxable; $25,001–$34,000 = up to 50% taxable; Over $34,000 = up to 85% taxable.

- Married filing jointly: Up to $32,000 = 0% taxable; $32,001–$44,000 = up to 50% taxable; Over $44,000 = up to 85% taxable.

3. Strategies to Mitigate Taxes:

- Diversify Income Sources:

- Save & invest in a mix of taxable, tax-deferred, and tax-free accounts (e.g., Roth IRAs, traditional IRAs, and taxable accounts).

- Diversify income sources to reduce provisional income and limit the taxation of Social Security benefits.

- Leverage Tax-Efficient Accounts:

- Use tax-advantaged accounts like Roth IRAs for withdrawals, as they are not included in provisional income calculations.

- Consider tax-free investment income sources such as municipal bonds.

- Strategize Withdrawal Timing:

- Plan withdrawals strategically to keep taxable income below thresholds that trigger higher taxation of Social Security benefits.

- Delaying Social Security benefits can reduce taxable income early in retirement and increase future benefits.

- Boost Portfolio Longevity:

- Mitigating taxes can extend the longevity of retirement portfolios, which is increasingly important as life expectancy rises.

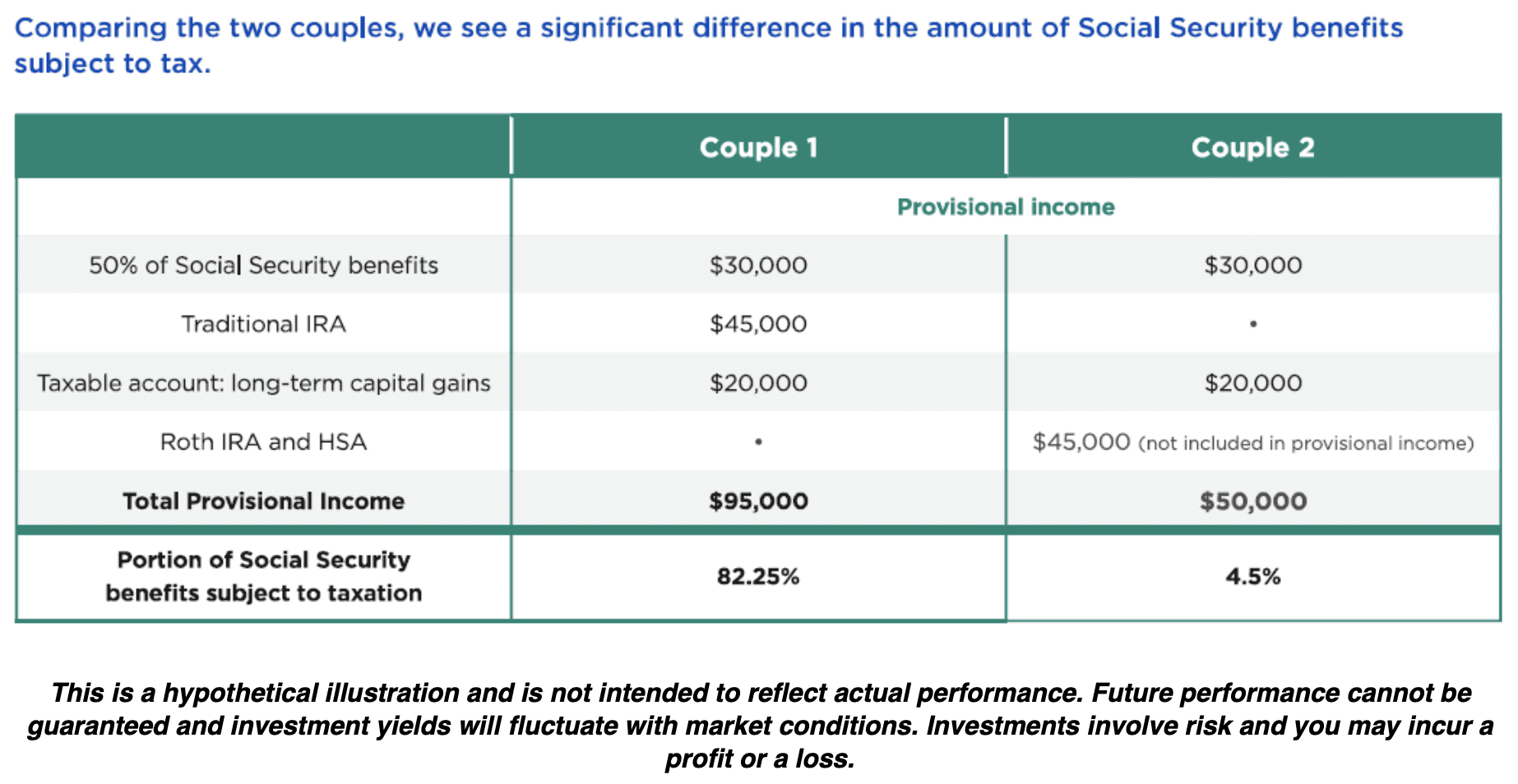

4. Case Studies demonstrated:

- Couple 1: With a higher provisional income ($95,000), nearly $50,000 of their $60,000 Social Security benefits are taxable due to withdrawals from a traditional IRA and taxable accounts.

- Couple 2: By using a Roth IRA and taxable accounts, their provisional income is reduced to $50,000, making 95% of their Social Security benefits tax-free. Additionally, they owe $0 in long-term capital gains taxes due to staying in the 0% tax bracket.

By implementing some of these strategies in retirement, including withdrawal sequencing strategies, retirees could potentially mitigate their tax burden, maximize their Social Security benefits, and extend the longevity of their retirement portfolios.

** Effective in 2026 (through 2028), it’s important to note that the One Big Beautiful Bill has changed much, reducing income tax for many Social Security recipients by introducing a new, additional standard deduction (subject to MAGI phase outs) of up to $6,000 for single filers and $12,000 for married couples aged 65+. These increased deductions act as a significant tax break, which will eliminate income taxes on Social Security benefits for many seniors. It’s important to consult with your Tax Advisor.

Edward Lynch, MBA, AAMS®, AIF® – Private Wealth Advisor

President & CEO, Lynch Wealth Strategies, Inc.

Army Lieutenant Colonel (Retired) – 28 Years of Military Service

3 Coates Drive, Suite 5, Goshen, NY 10924 – 845-294-3456

www.LynchWealthStrategies.com | Edward.Lynch@raymondjames.com

The material is general in nature. Securities offered through Raymond James Financial Services, member FINRA / SIPC. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. Lynch Wealth Strategies is not a registered broker/dealer and is independent of Raymond James Financial Services.

Private Wealth Advisor is a designation awarded by Raymond James to financial advisors who have demonstrated mastery in anticipating and managing the expansive financial needs of high-net-worth individuals, families and organizations.

Every investor’s situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Please note, changes in tax laws may occur at any time and could have a substantial impact upon each person’s situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

This material is being provided for information purposes only. The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Edward Lynch and not necessarily those of Raymond James.

401(k) Plans: 401(k) plans are long-term retirement savings vehicles. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty.

IRAs: Contributions to a traditional IRA may be tax-deductible depending on the taxpayer’s income, tax-filing status, and other factors. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty.

Roth IRA: Like Traditional IRAs, contribution limits apply to Roth IRAs. In addition, with a Roth IRA, your allowable contribution may be reduced or eliminated if your annual income exceeds certain limits. Contributions to a Roth IRA are never tax deductible, but if certain conditions are met, distributions will be completely income tax free. Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are per.